Could you be owed £1,658** in car finance compensation?

**The FCA currently estimates that most individuals will receive an average of £829 in compensation per agreement. On average we find 2 car finance agreements per client, giving a potential claim value of £1,658.

It takes as little as 60 seconds to check

Here's how it works

We'll find your finance agreements

Our system securely connects with trusted credit agencies and vehicle records to find your car finance agreements, even if you've moved house or changed your name. It's only a soft credit check, so your credit file won't be affected.

We'll review your eligibility

After you enter a few basic details, our system searches for your past car finance agreements, including those dating back to 2007, where available.

Driving you safely to the next stop

Once your finance agreements are found, Mis-sold will review your agreements in detail, we'll either do this ourselves or send it to one of our partner law firms. You will be updated every step of the way while we collect evidence, negotiate directly with the lenders, and fight your case for you.

You can claim without using a claims management company, to your finance provider and then to Financial Ombudsman Service (FOS), for free. The FCA is introducing a free consumer redress scheme.

Could your car finance

have been mis-sold?

Some agreements included commission setups that weren't always made clear at the time.

If you had a PCP or HP agreement between April 2007 and November 2024, you may have been affected by one of the following:

Discretionary Commission Arrangements (DCAs)

The interest rate could be increased, and that increase could boost dealer commissions.

Unfairly High Commission Charges

The commission paid may have been disproportionate to the finance agreement.

Contractually Tied Arrangements

The broker may have been tied to one lender, rather than comparing options fairly.

Real customer stories

What our customers say about the process.

Frequently asked questions

The answers you need about the claims process, fees, and more.

Latest News

Get the latest updates on car finance, industry changes, and expert viewpoints.

Blue Motor Finance Under Pressure As FCA Compensation Costs Shake The Industry

Blue Motor Finance has moved into the spotlight after reports suggested the lender could be facing serious financial pressure linked to the FCA’s motor finance compensation scheme.

BMW Car Finance Claims In 2026: Understanding The FCA Redress Scheme

BMW became one of the UK’s most heavily financed car brands during the rise of PCP agreements throughout the 2010s. Monthly payment advertising, upgrade cycles and dealership finance packages made it easier for many drivers to move into newer BMW models without paying the full purchase price up front.

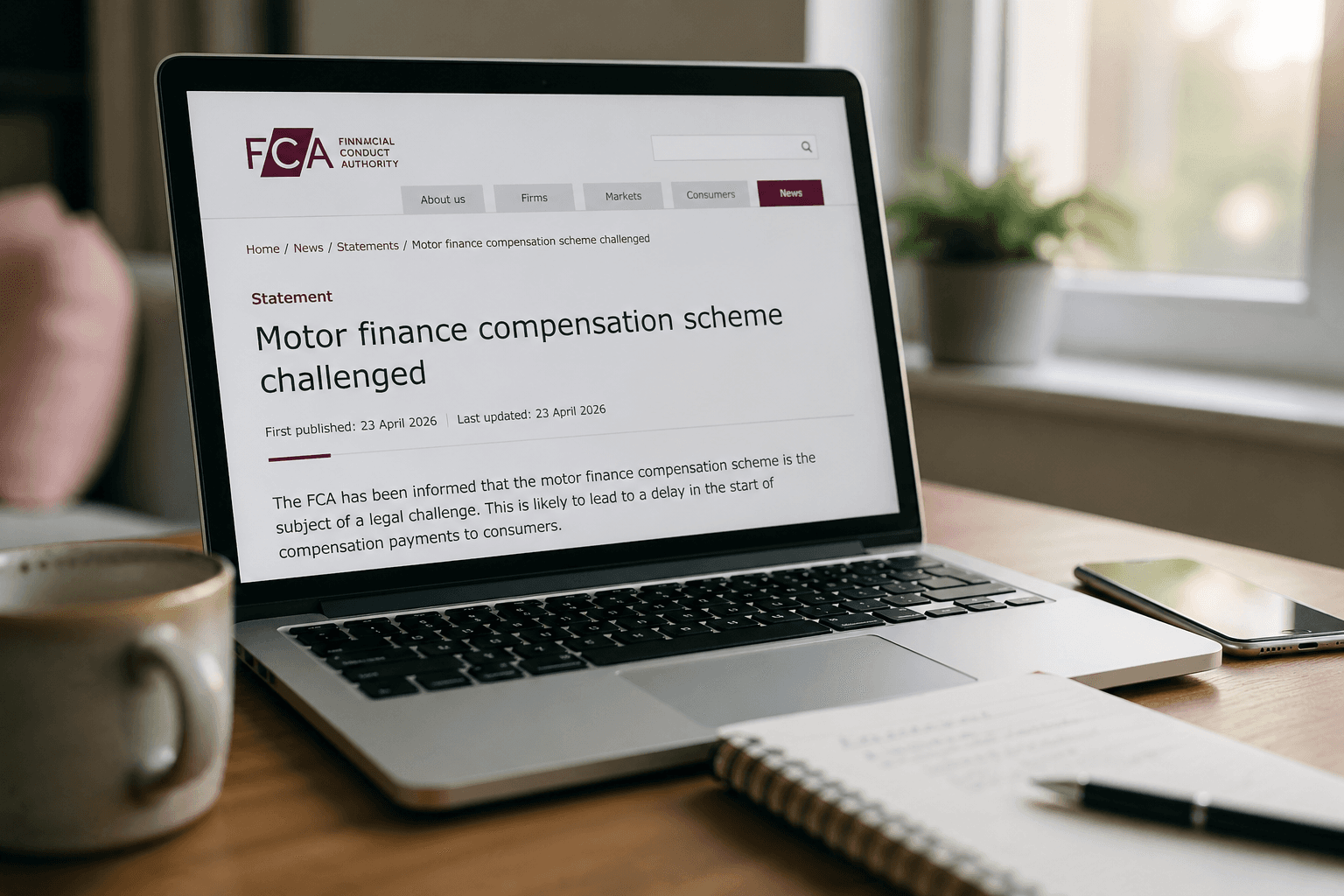

FCA Motor Finance Compensation Scheme Challenged

The FCA’s motor finance compensation scheme has now been challenged, which is likely to delay payouts and may extend how long you have to make a claim.