Why Subprime Car Finance Customers Are Most Likely to Be Mis-Sold

Understanding Subprime Car Finance

Subprime car finance helps many people access a car when their credit history is poor or limited. For some, it is not a fallback option. It is the only realistic way to get a vehicle.

There is nothing inherently wrong with subprime lending. Higher-risk lending is allowed under FCA rules. Problems arise when the finance is not explained properly or when customers are steered into agreements they do not fully understand. That risk can be higher where you already feel you have little choice.

The Financial Conduct Authority expects lenders and brokers to treat all customers fairly, regardless of credit score. Where customers may be more vulnerable, firms are expected to take extra care, not less.

What Subprime Car Finance Means in Practice

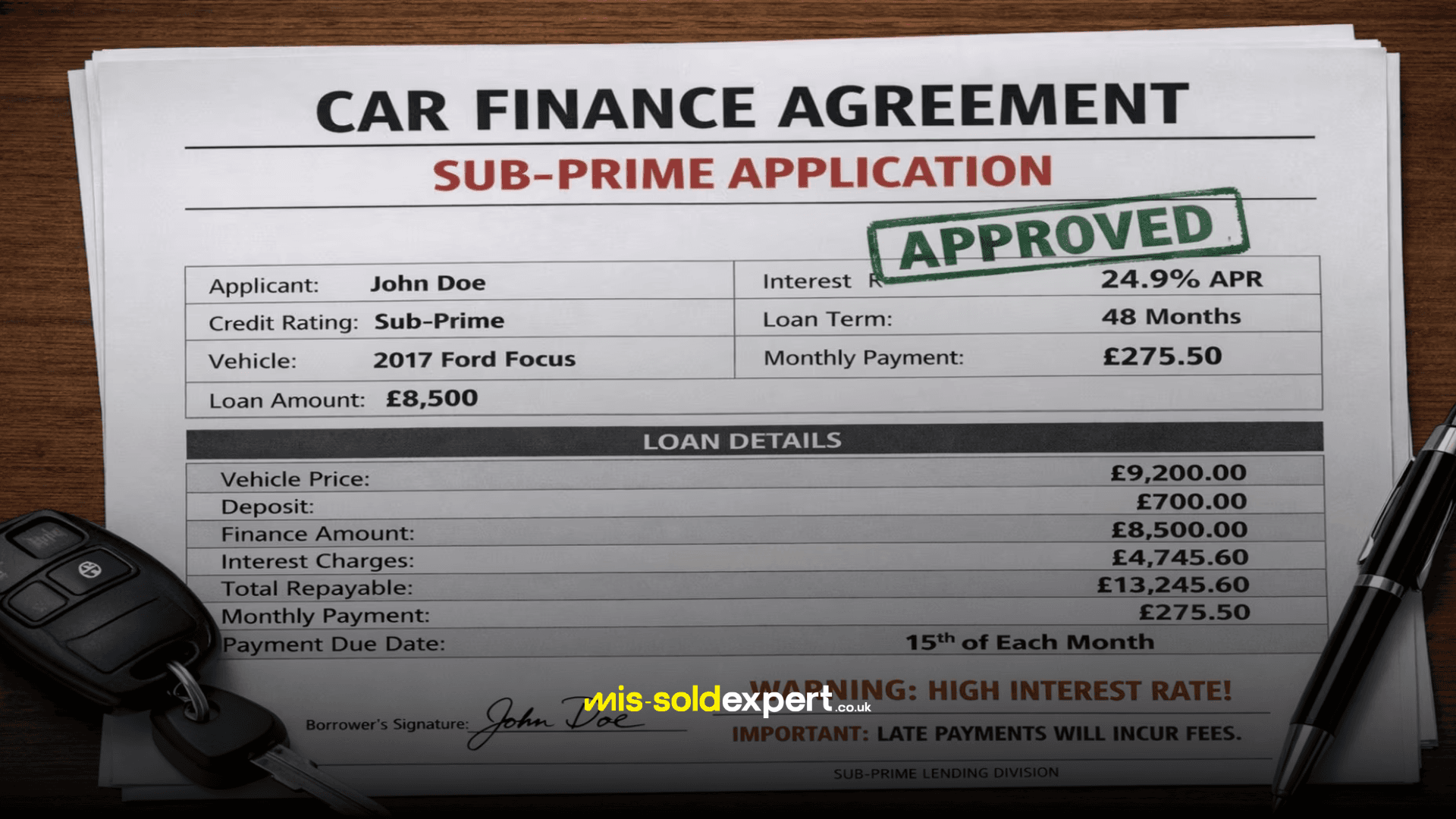

Subprime car finance usually applies where you have missed payments, defaults, a low credit score, or a limited credit history. Because lenders see this as higher risk, interest rates are often higher than mainstream finance.

A higher interest rate on its own does not mean the finance was mis-sold. FCA rules allow firms to price for risk. What matters is whether the agreement was explained clearly and whether you understood the full cost before signing.

The real issue is not the monthly payment. It is the total cost over the life of the agreement. A payment that looks affordable can hide a much higher overall cost if interest, fees, and the length of the agreement are not properly explained.

Why Subprime Customers Can Face Higher Risk

When you apply for subprime finance, it is common to feel on the back foot. If you believe your options are limited, you may feel pressure to accept what is offered without questioning it.

Some customers may also feel less confident asking questions or may have less experience with finance products. The FCA recognises that vulnerability is not just about personal circumstances. It also includes confidence, understanding, and financial pressure.

Where vulnerability exists, firms are expected to slow the process down, check understanding, and provide clearer explanations. Rushing a customer through a complex agreement increases the risk of unfair outcomes.

Where Mis-Selling Commonly Occurs

Mis-selling issues in subprime car finance often relate to how information is presented. Common concerns include:

- A strong focus on monthly payments, with little explanation of the total cost

- Interest rates are not being clearly explained or compared

- Key features or risks of the agreement being downplayed

- Alternative finance options are not being discussed at all

Commission can also be relevant. The Commission itself is not banned. However, FCA rules are clear that commission must not lead to unfair outcomes. If incentives influence how a product is presented, and that influence is not transparent, the fairness of the sale may be questioned.

Pressure, Urgency, and Limited Choice

Pressure is a common concern in subprime sales. You may feel that refusing an offer means losing your chance to get a car altogether.

Sales approaches that rely on urgency, or that suggest there are no other options, can undermine genuine choice. Being pushed to decide quickly rarely supports informed decision-making.

The FCA expects firms to give you time to consider your options, particularly where agreements are long-term or complex.

FCA Expectations on Fair Treatment

The FCA requires firms to communicate in a way that supports understanding. This includes explaining key terms, costs, and risks in plain English.

Where customers may be vulnerable, firms are expected to adapt their approach. That may involve spending more time explaining the agreement or checking that you understand it before proceeding. Failing to do so increases the risk of mis-selling.

Poor Credit Does Not Mean Lower Standards

A common misconception is that mis-selling is about credit quality. It is not.

Having poor credit does not reduce your right to fair treatment. Subprime customers are entitled to the same standards of transparency, care, and fairness as any other consumer.

Lower creditworthiness does not justify lower standards.

What to Do If You Have Concerns

If you are concerned about how your subprime car finance was sold, you can complain directly to the lender. It can help to focus on:

- What you were told at the point of sale

- What was not explained clearly

- Whether you felt pressured or rushed

- Whether you understood the total cost and key terms

Complaints are assessed on their individual facts, based on the regulatory standards that applied at the time of the sale.

Subprime car finance can be legitimate and necessary. When handled properly, it can help people move forward. When it is not, problems can arise. Clear communication, transparency, and fair treatment are not optional. They are central to FCA expectations and consumer protection.

If you believe your car finance may have been mis-sold, Mis-Sold Expert can explain the complaints process and your options.

You can claim without using a claims management company; you can go to your finance provider and then to FOS, for free. Additionally, the FCA is introducing a free consumer redress scheme.