Average Car Finance Payout of £829 Per Agreement Confirmed

The Financial Conduct Authority has finally confirmed the compensation figures for mis-sold car finance, giving much needed clarity to an issue that has affected millions of people across the UK.

For years, concerns have been building around how car finance was sold, particularly around commission arrangements that weren’t properly explained. Many people agreed to finance without knowing how brokers were paid, or that those payments could impact the cost of their loan. Now with the FCA’s final rules in place there’s a clear framework for how compensation will be calculated, who will be included and what this means for you in practical terms.

This isn’t a minor regulatory change. It’s one of the biggest consumer redress exercises ever carried out in the UK. The numbers are huge but understanding how they apply to your own agreement is what really matters.

The Confirmed Compensation Figures

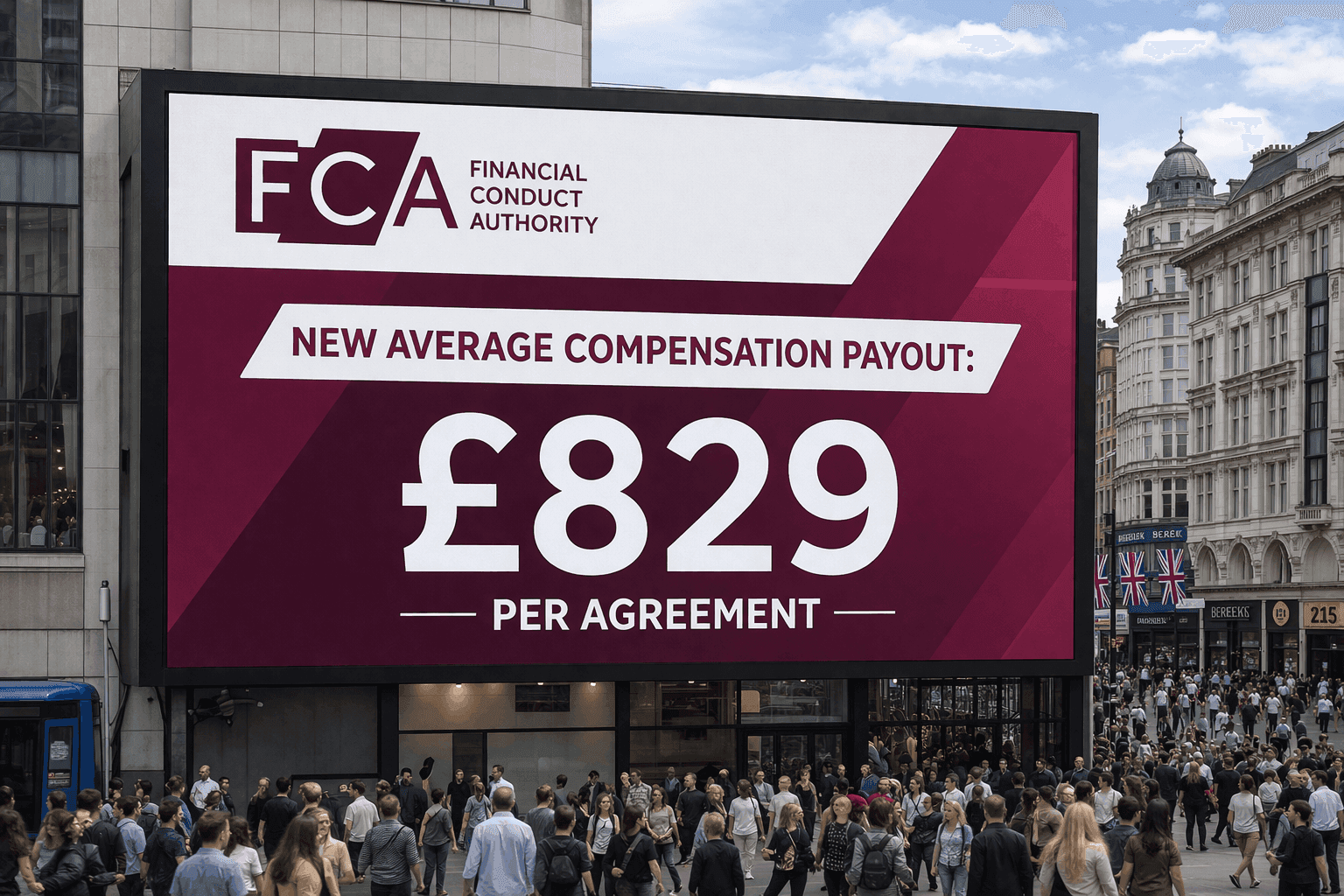

The FCA has published the overall numbers. They estimate £7.5 billion will be paid in compensation across 12.1 million agreements. The average payout is £829.

These figures give you an understanding of the scale of the issue however, they’re not fixed outcomes. The average is based on modelling across a wide range of agreements and individual payments will vary depending on the details of your case.

Some people will get less than the average stated, others will get more. It all depends on how the finance was arranged, how much commission was involved and how long the agreement ran for.

Why Compensation Is Being Paid

At the heart of the FCA’s findings is a lack of transparency.

Many customers weren’t told commission was being paid at all, let alone how it worked. In some cases brokers could increase the interest rate and earn more commission as a result. This created a clear conflict where the person arranging your finance could benefit from making it more expensive.

The FCA found this wasn’t an isolated issue. It was widespread across the market and often not explained in a way that allowed customers to understand what was happening.

There were also cases where commission levels were high, or where relationships between lenders and dealers limited the options without being clearly disclosed. Taken together this meant many people entered into agreements without having the full picture.

That’s why the FCA concluded some of these arrangements created an unfair relationship.

What the Average Payout Actually Means

The £829 figure is useful but can be misleading if taken at face value.

It’s just an average across approximately 12.1 million agreements, all with different values, structures and terms, meaning there’s a wide range of possible outcomes.

Someone with a small loan over a short period where commission played a limited role may get a lower amount or no compensation at all, whereas someone with a larger agreement, higher commission and a longer term may get a larger payment.

The FCA expects this variation. The scheme is designed to reflect the specific details of each agreement rather than apply a one-size-fits-all amount.

How Compensation Is Calculated

To keep things consistent the FCA has introduced a standard method that firms must follow when calculating compensation.

In most cases this involves looking at two things. The first is an estimate of the financial loss, which reflects how much extra you may have paid because of the way the finance was arranged. The second is the commission that was actually paid as part of your agreement.

These two figures are combined and averaged and interest is then added on top.

The FCA uses different assumptions depending on when the agreement was taken out. For agreements after April 2014 the model uses a lower adjustment to reflect more recent market conditions. For earlier agreements the adjustment is higher because the FCA considers the potential harm to have been greater during that period.

In more serious cases, particularly where commission was very high and not disclosed clearly, a different approach may apply. Instead of averaging the figures the full commission paid may be returned, along with interest. These cases are less common but can lead to higher payouts.

At the same time the FCA has built in limits to ensure outcomes are proportionate. Where the overall cost of credit was already low or where commission was minimal compensation may be reduced or not payable at all.

Interest and the Time Factor

Any compensation paid will include interest to reflect the fact you were out of pocket.

The FCA has set a standard approach based on the Bank of England base rate plus an additional one percent. It has also introduced a minimum of three percent per year to ensure compensation remains fair even during periods when interest rates were very low.

This means the longer ago the agreement was the more interest may be added, although the exact amount will depend on the timing and structure of the loan.

What This Means in Practice

For many people the outcome will be a relatively small payment totalling £829 or less.

More importantly the scheme removes much of the uncertainty that would come with pursuing a claim individually. Instead of relying on complaints or legal action there is now a clear process that firms must follow.

For some consumers, especially those with higher commission arrangements, the outcome could be more significant. The key point is the scheme is designed to reflect both the financial impact and the lack of transparency that led to it.

When You Can Receive Your Compensation

Timing depends on your individual situation.

If you’ve already made a complaint your case will be reviewed first. You may hear back within a few months of the scheme going live and some payments are expected towards the end of 2026.

If you haven’t complained your lender may contact you if your agreement is affected. This process may take longer with many cases progressing through 2027.

The FCA expects most claims to be resolved by the end of that year although some may run slightly longer depending on when they are identified.

Why the FCA Took This Approach

The FCA could have allowed each case to be handled individually through complaints or the courts. That would have resulted in delays, inconsistent decisions and higher costs.

Instead it introduced a structured scheme with clear rules and timelines.

This approach is designed to make the process more efficient and more consistent while still delivering fair outcomes for consumers. It also gives firms a clear framework to follow which helps avoid the uncertainty that comes with case-by-case disputes.

What You Need to Know

The confirmed compensation figures are useful but they are only part of the picture.

The average payout of £829 is not what everyone will get. Your outcome depends on your own agreement and how it was arranged.

The key issue is whether you were given clear and fair information at the time. If important details about commission or the structure of the deal were not explained properly your agreement may fall within the scope of the scheme.

Understand Your Agreement

Many people are unsure how their car finance was structured or whether commission was involved.

You can check your car finance agreement with Mis-Sold Expert to understand how your deal was set up and whether any of the issues identified by the FCA apply to you. We explain the key details in plain English so you can see how your agreement works and what it means for you.

Gain Clarity with Mis-Sold Expert

Check your car finance agreement with Mis-Sold Expert. We’ll explain how your deal was set up and if commission was involved in plain English. Stay up to date with the latest FCA news and industry updates.

You can claim without using a claims management company; you can go to your finance provider and then to FOS, for free. Additionally, the FCA is introducing a free consumer redress scheme.